Markets are booming but strains show in the economy

Is there a disconnect between market performance and economic activity?

Equity markets are booming. The S&P 500 is up 7% year-to-date and has risen 16 of the past 18 weeks, something that hasn’t been seen since 1971. The so-called Magnificent Seven are the talk of the town, as key drivers to the upwards move. These stocks are up 92% since the start of last year, versus the rest of the S&P 500, which has increased by 17%.

Yet, the Magnificent Seven may soon turn into the Magnificent Four, as the performance of the companies start to diverge. Three stocks, in Alphabet, Apple, and Tesla, have fallen this year. Tesla is the worst performer in the S&P 500 this year.

Apple and Tesla are being hurt by slowing China sales, a combination of a teetering economy there as well as both losing market share to local competitors. Meanwhile, Alphabet is being seen as behind the ball on AI compared to the likes of Microsoft and Amazon.

Frothiness is reaching other areas of market, with artificial intelligence server maker, Super Micro Computer, becoming the latest meme stock, rising 278% this year, surpassing its climb of 223% in 2023. The meteoric jump has led to the stock being included in the S&P 500 index. Who said indexes are passive?

Super Micro Computer now sports a market capitalization of US$61 billion, and it’s valued at a cool 84x earnings and on an EV/Ebitda multiple of 66x.

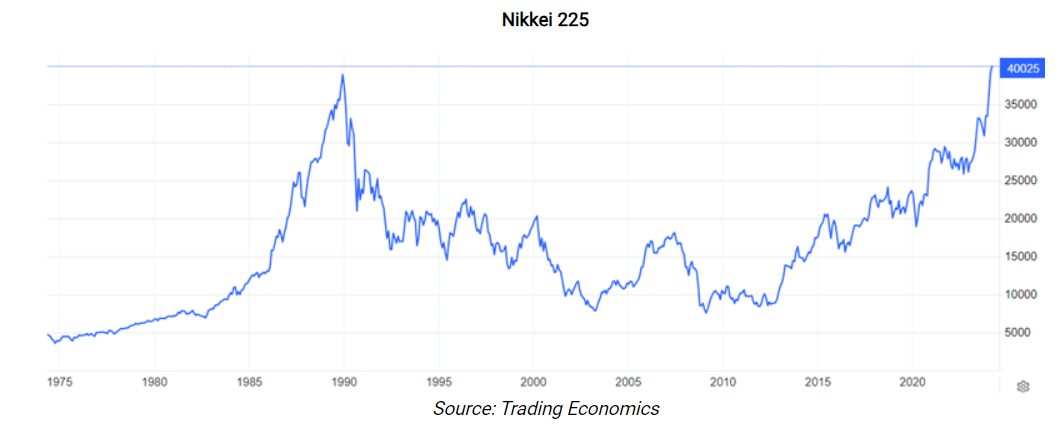

And the optimism is reaching other markets too. This week, Japan’s Nikkei 225 crossed 40,000 for the first time ever, after breaching its 1989 record high in late February.

Outside of equities, other markets are feeling the love too. Bitcoin has jumped 61% this year, after a 156% gain in 2023.

And the optimism is reaching other markets too. This week, Japan’s Nikkei 225 crossed 40,000 for the first time ever, after breaching its 1989 record high in late February.

Outside of equities, other markets are feeling the love too. Bitcoin has jumped 61% this year, after a 156% gain in 2023.

Even the proverbial ‘pet rock’, gold is scaling all-time highs. It’s surged 5% this month and 17% over the past year in US dollar terms.

Optimism doesn’t stretch to economies

Much of the positivity in markets isn’t filtering down to economies. The world’s third largest economy, Japan, is already in recession. The fourth largest, Germany, will almost certainly join it when first quarter GDP statistics are released. Meanwhile, the second biggest economy, China, remains in the sick bay as its credit-fuelled property bubble deflates.

The UK has also recently joined the list of those in recession, along with Sweden, Ireland, and Finland. France, Spain, Italy, New Zealand, and Israel are expected to join them soon too.

Meanwhile, Australia isn’t in great shape either. GDP data released this week shows the economy here expanded by 0.2% during the December quarter. Meanwhile, annual GDP growth slowed to 1.5%, the lowest in 23 years.

GDP was only in the black thanks to strong population growth. Per capita (or per person) GDP fell 0.3% during the quarter and was 1% down on the year. It’s the third consecutive quarterly decline in per capita GDP. So, we’re officially in a per capita recession.

The big culprit for the poor economic data is a struggling consumer. CBA has this to say on the matter:

“Growth in real consumer spending over the past year has been incredibly weak given the squeeze in real household disposable income … Real household consumption grew by just 0.1%/qtr in Q4 24 [ed: this should read Q4 23] and is up by the same amount over the year. In other words aggregate consumer spend has essentially been flat for a year.

On a per capita basis real consumer spending is down by a very large 2.4% over the year. Such an outcome would normally be associated with a large negative shock or recession. The weakness in the consumer lies at the heart of the soft GDP outcomes. And it is the primary reason why the unemployment rate is on a firm upward trend (albeit from an incredibly low level).”

Spending on essentials increased 0.7% during the December quarter, but this was largely offset by discretionary spending declining by 0.9%. The data shows that people are cutting back on dining out, recreation and clothing.

It appears that savings built up from the pandemic period have been exhausted and people are reducing their spend on non-essentials to pay for essentials such rents, food, health, and electricity.

One curiosity is the extreme divergence between the data on consumer spending and the positive results and outlooks reported by consumer discretionary companies during the recent reporting season. Hugh Dive looks at this and all the earnings results in his article this week.

The other question that comes out of this GDP print is what it means for the RBA and rates moving forward. Could it be that the RBA is forced to cut rates before the Fed in the US? It’s an intriguing possibility, though time will tell.

Why are markets soaring, while economies are flailing?

The one major economy that’s firing on all cylinders is the US. Buoyant consumer spending from Millennials, exploding industrial construction as domestic manufacturing moves onshore from China, and strong government spending, are driving an acceleration in economic growth.

The outlook for the US economy looks reasonable as well, given positive demographics, further onshoring of manufacturing, relatively cheap energy sources, and it being the world’s major technology innovation hub.

That contrasts with economies in Europe, North Asia, and China where populations are quickly ageing, domestic demand is stalling, energy prices are high, and innovation underwhelms versus America.

This perhaps explains why the US stock market has trounced most others over the past decade and continues to lead the way.

And even Donald Trump may not be enough to spoil that positive outlook…