Which ASX tech companies are best placed for the cost-cutting wave

Tech layoffs are accelerating as firms focus on profitability, but not all companies are set to benefit from cost-outs. We highlight two that are.

Mentioned: FINEOS Corp Holdings PLC (FCL), EML Payments Ltd (EML), WiseTech Global Ltd (WTC), Zip Co Ltd (ZIP)

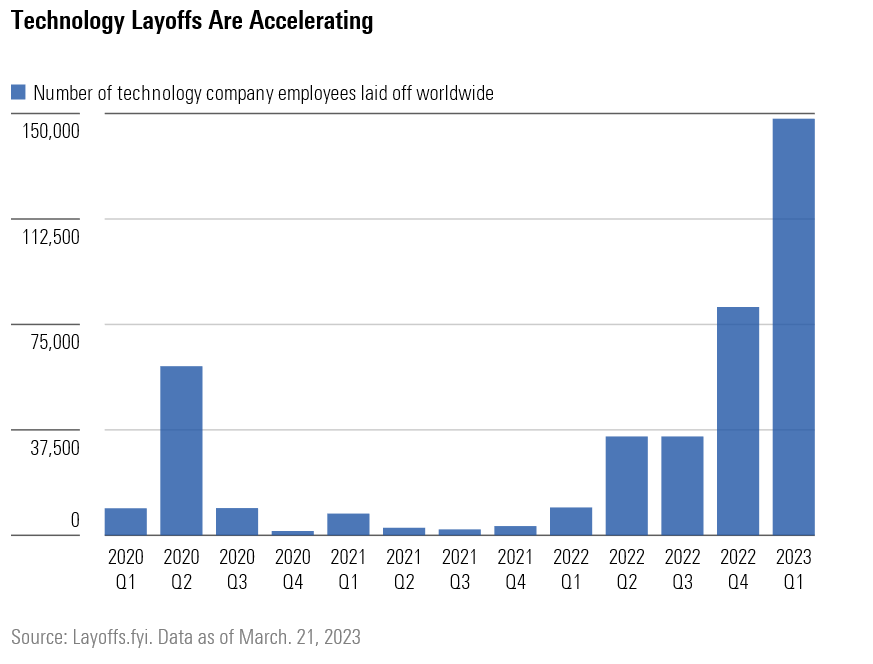

A shift in focus from growth to profitability in the tech sector has triggered a wave of cost-cutting measures — but not all companies are well placed for the push towards profits.

In Morningstar’s most recent Quarterly Outlook Report—which is available in full to Investor subscribers here—Morningstar analyst Adrian Atkins laid out a sector-by-sector overview.

“The real estate and financial services sectors screen as most undervalued after selloffs caused by market fears of contagion from bank and REIT failures in the US and Europe,“ he says.

Atkins also points to the technology sector—as well as energy and communication services—as other areas of the market which stand out with a high proportion of undervalued stocks.

Among the sectors listed above, technology has been one of the stronger performers year-to-date, with the Morningstar Australia Technology Index outperforming the Morningstar Australia Index.

While the sector has performed strongly year-to-date, after it was hit hard in early 2022, Morningstar analyst Roy van Keulen says there has been a noticeable shift in investor sentiment away from previously popular but unprofitable tech companies.

“Markets initially encouraged technology companies to hire aggressively with the pandemic to grow, but the mood has decidedly shifted,“ he says.

“The market now praises tech companies announcing layoffs and punishes those who don’t.”

Cost-cutting measures like layoffs have spiked since the start of the year. However, despite some tech companies now moving through second-round layoffs, van Keulen says that most of the headcount added since the pandemic remains and foresees further cuts ahead.

“We expect further cost cuts in the technology sector through 2023,” he says.

But cost-cuttings will not impact the sector uniformly, says analyst Shaun Ler, pointing to fintech start-ups Zip (ZIP) and EML Payments (EML) as two tech companies in a disadvantaged position for the cost-cutting push.

“The fintechs are similarly focused on improving profitability, though this won’t help to generate maintainable earnings for all firms alike.”

“For no-moat, capital-intensive businesses such as Zip, the rush to boost profitability is required given external funding challenges and rising interest costs,” he says.

“Unfortunately, cutting costs, particularly on customer acquisition, risks market share losses."

“Similarly, for troubled firms like EML, cost-outs are necessary to offset downsides from higher remediation costs that befell the firm due to its regulatory missteps,” he says.

Two ASX tech companies with moats

In contrast to fintechs like Zip and EML Payments, van Keulen and Ler highlight two tech companies which hold a “narrow” or “wide” Morningstar economic moat rating and are well placed for the sector’s profitability push.

A Morningstar Economic Moat Rating represents a company's durable competitive advantage. A company with an economic moat is expected to fend off competition and earn high returns on capital for either 10 years (in the case of a narrow-moat rating) or 20 years (in the case of a wide-moat rating).

Fineos (FCL)

- Star rating: ★★★★★

- Fair value estimate: $3.40

- Economic rating: Wide

Ler says insurance software developer Fineos (FLC) is one moated company well poised for the push to profitability.

“We don’t expect cost-outs to harm market share and dampen the earnings power for firms such as Fineos.”

“Fineos' cost-cutting plans are largely aimed at reducing unnecessary costs and lessening wage inflation and shouldn't impede growth”

While Fineos still remains unprofitable, Ler notes that the company reinvests to solidify switching costs with sticky customers, to help new business wins, and to maintain its lead over would-be competitors—resulting in a positive outlook.

“We anticipate share gains from more product holdings per client, new client adds, and expansions into new regions and adjacent markets such as medical, dental, and vision,” he says.

“There are also opportunities for cost efficiencies from client transitions to the cloud, automation, and use of emerging economy staff.”

All that said, Fineos has been hit hard by the shifting investor sentiment noted above, with shares selling-off substantially earlier this year following its half-year report.

The sell-off pulled Fineos’ share price down more than a third in the space of a week, but Ler says the company may have been punished too harshly.

“The recent poor first half strikes us as a blip, and we believe the market’s concerns are unlikely to play out.”

“Revenue growth is currently soft and the market is punishing Fineos heavily. However, we think this is temporary, reflecting a move to cloud-based software, which brings the promise of a more valuable recurring revenue stream longer-term.”

WiseTech Global (WTC)

- Star rating: ★★★★

- Fair value estimate: $90.00

- Economic moat: Narrow

Narrow-moat WiseTech Global (WTC)—which develops software solutions to the global logistics industry—was another top pick among tech stocks.

“WiseTech presents a rare combination of a large, highly winnable addressable market with attractive unit economics,” says Van Keulen

A strong half-year report in February pushed Morningstar’s fair value estimate up 2%, with van Keulen saying the company was on track to become the operating system for global logistics.

“Our view differs from the market as we believe WiseTech provides the technology to help logistics companies outperform their competition,” he says.

“Given that the market for logistics services naturally selects for the lowest-cost providers and given the cost-advantages that CargoWise provides, we have high confidence that this solution continues to be adopted by more customers.”

While most of the sector hired up during the pandemic, van Keulen says WiseTech chose a different approach.

“Whereas most the technology grew headcount in line with abnormally strong revenue growth and is currently forced into making layoff, WiseTech’s headcount was mostly flat through the pandemic and it is currently hiring aggressively,” he says.

“Similarly, for acquisitions, WiseTech has made viturally no aquisions through the pandemic and is currently, perhaps opportunistically, making large acquisitions while valuations in the technology sector have come down. ”

Shares in WiseTech are trading around $65 per share, a 27% discount on Morningstar’s fair value estimate of $90.00.