Woodford: a cautionary tale for Australian investors

Neil Woodford's fall from grace holds lessons for Australian investors.

In this first of a two-part series, we explain the rise and recent fall of rock-star UK fund manager Neil Woodford and his Woodford Equity Income Fund.

Imagine you put your children's savings into a fund to invest for their future.

You choose a well-known fund manager with a good track record of delivering strong returns.

Then suddenly the fund goes through a period of sustained poor performance, and investors start to pull their money. You consider transferring your money out, but decide to take the long view.

And then, the fund tells you it's suspended trading and you can't take your funds out.

This unfortunate situation is a reality for Ruth from South London. She is one of thousands of investors who has their money locked in the Woodford Equity Income fund.

The fund, run by one of Britain's top investment managers, was suspended earlier this month after an increasing number of clients demanded their money back.

“[The fund] seemed like a good building block; the kind of fund where I could invest my money and then forget about it for the next few years," Ruth told Morningstar UK journalist Emma Simon.

Ruth said she saw Wooford as a “safe pair of hands”.

Morningstar Australia fund analyst Andrew Miles says there are lessons Australian investors can learn from the Woodford debacle.

First, what went wrong for Woodford.

What happened

High profile manager Neil Woodford was thought of as Britain's answer to legendary investor Warren Buffett.

After almost 30 years with UK investment giant Invesco Perpetual, the star stock-picker – who had amassed more than £30 billion in funds under management – famously left the firm in 2014 to set up his own business and launch the flagship Woodford Equity Income fund.

The Invesco Perpetual funds he left behind – Income and High Income – bled billions in assets as many investors who had enjoyed great success under his watch loyally followed him to his new venture. And, for a while, their decision served them well.

“Investors who moved over to Neil Woodford’s new fund after he left Invesco would initially have been over the moon," Laura Suter, personal finance analyst at AJ Bell told Morningstar UK journalist Holly Black.

"On its three-year anniversary, the Woodford Equity Income fund was way ahead of its peer group as well as the Invesco funds Woodford previously managed.”

Indeed, three years after launch, the Woodford fund had returned a meaty 39.3 per cent compared to an average of 19.4 per cent from the UK Equity Income sector, cementing the fund's cult status.

Morningstar UK associate director Peter Brunt says outperformance was driven primarily by making astute long-term macro calls and strong stock selection.

Cracks begin to appear

But in 2018, the star stock picker was brought back to earth. Woodford's notoriously contrarian style struggled as global stock markets soared and several stock-specific issues hammered performance, including companies Capita, Provident Financial, Allied Minds and Prothena.

Woodford Equity Income was down 13.6 per cent in the year to 30 June 2018. Meanwhile the average UK Equity Income fund was up 2.5 per cent.

Growth Chart (GBP): Woodford Equity Income C Sterling Acc v Category Benchmark

Source: Morningstar Direct

Investors piled out of Woodford’s flagship fund in droves. Assets under management shrunk from more than £10 billion to £6.5 billion.

The fund was also dropped from a number of broker best buy lists and downgraded by Morningstar analysts to a Bronze rating.

Morningstar's Brunt remained broadly positive on Woodford overall, but raised several concerns about the fund's investment mix and positioning.

Firstly, while Woodford had previously targeted the same kind of opportunities as the Invesco fund – global companies with diversified revenue streams –by early 2017, it had shifted towards more domestically-focused names and early stage companies, especially healthcare firms exploring new drugs and treatments.

"With these typically being smaller in size, the market-cap of the portfolio saw a striking evolution – within the listed portfolio of the portfolio, small cap and mid-caps accounted for 40 per cent in January 2016, by the end of March 2019, they stood at 95 per cent," says Brunt.

Woodford takes extreme action

"Despite Woodford's view that the UK economy was improving being largely correct, the strategy experienced prolonged underperformance, with persistent stock-specific problems among the quoted portion of the portfolio a key impact," says Brunt.

Continued redemptions and the delaying of several unquoted names from IPO forced the group to take extreme action to keep the unquoted exposure below the regulatory 10 per cent limit in the first quarter of 2019.

Outflow of cash becomes a torrent

As investors grew increasingly frustrated with poor performance, the fund continued to experience redemptions.

Woodford Equity Income was among the worst performers of all funds in May 2019, down 9.1 per cent in the month. Concerns also mounted about the proportion of the fund invested in illiquid assets and early-stage biotech companies.

May was the 23rd consecutive month that the Woodford Equity Income fund had suffered net outflows. It is estimated that investors pulled around £10 million a day out of the fund in May.

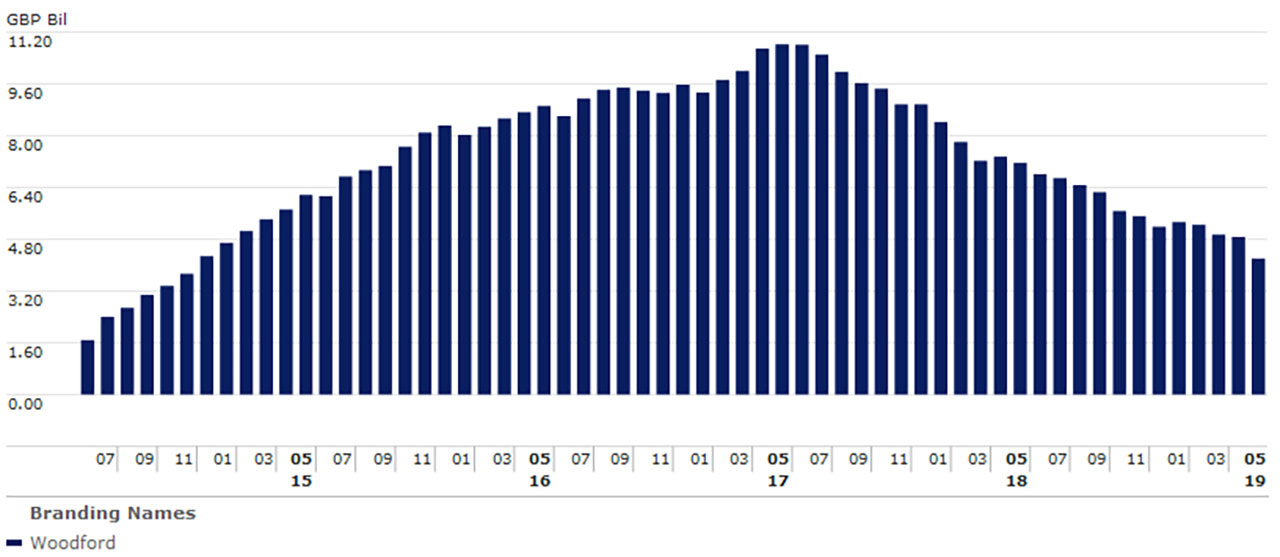

Asset flows by brand name: Woodford

Source: Morningstar Direct

The size of the fund, which peaked at £10.2 billion, shed £560 million of assets in a matter of weeks. Today it has £3.7 billion of assets.

Investors trapped

Then on June 3, when the levels of redemptions accelerated to unmanageable levels, the group was forced to suspend dealing. This was aimed at heading off a fire sale of assets to meet immediate liquidity demand, says Brunt.

This meant any investors remaining in the fund were unable to liquidate their holdings, with no choice but to stay invested. They're also still paying fees.

Neil Woodford has issued a YouTube apology to investors whose money remains frozen in the fund.

Morningstar analysts have now downgraded the Woodford Equity Income fund to a Negative rating.

Part 2: Lessons Australian investors can learn from the Woodford debacle

This article was compiled by Morningstar Australia reporter Emma Rapaport from a collection of Morningstar UK editorial and fund research.