Investing basics: Make $1 million before retirement

Hitting the million-dollar mark before retirement is possible if you start early enough and follow a disciplined investment strategy, writes Emma Rapaport.

Australians have long been told that having $1 million in savings is needed for a worry-free retirement. But for a lot of people, that sounds like a Herculean task.

If you plan to use a cash account returning close to 2 per cent interest, then yes – you'll need a lot of savings to achieve your million-dollar target, and will likely endure a very tight budget.

Harnessing the magic of compound interest by putting your savings in a superannuation fund – with the goal of having a million dollars in 30 to 40 years – is possibly a more appealing, effective option.

If you start saving early, it's actually easier to let your investments do as much heavy lifting as possible.

That's not to say you'll definitely reach $1 million, or that you even need that amount to retire comfortably – but let's have a look at what it would take.

Crunching the numbers

As you may know, the general concessional cap for contributing to super – the maximum amount before you must pay a higher tax rate – is $25,000 from 1 July 2017.

If your goal is to have a million dollars by the time you retire at age 65, the good news is that you don't need to save anywhere near that much per year, provided you start early. You can do the maths yourself using various free tools that are readily available, including the Australian Securities and Investments Commission's online compound interest calculator.

Below is an example of a 25-year-old who has not yet begun saving:

Amount saved at 25 $0

Amout wanted to have saved by 65 $1,000,000

Annualised return expectation 5% per year

Years until 65 40

Yearly contribution to super required $8,300

How will funds perform over 40 years?

How do I know what funds will return over the next 40 years? In truth, I don't, and anyone who says they do is lying. But it's possible to make a well-educated guess instead.

Here's how I came up with 5 per cent. Since the superannuation guarantee was introduced in 1992, the average long-term annual compound median return generated on a balanced-option super fund – comprising between 60 per cent and 80 per cent growth assets – was 7.6 per cent, after fees, for the 25-year period to 30 June 2017, according to Morningstar.

That's 5 per cent annually, on average, when you allow for inflation. This is referred to as the "real" return.

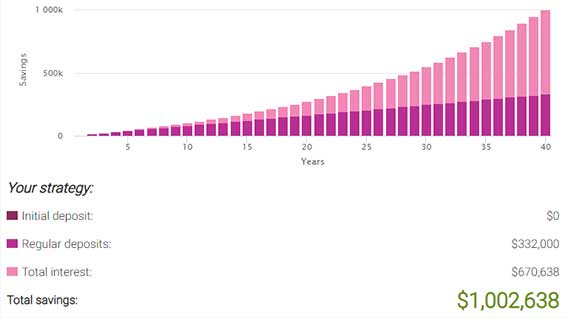

Image: Savings and investment strategy to reach $1m by retirement

Source: ASIC compound interest calculator

Does that mean balanced funds will return around 5 per cent every year into the future? Of course not – this is just the smoothed-out, average annual return over the past 26 years.

Reiterating my earlier point about not being able to predict performance, there is no accurate way to guess what markets will do over short-term periods. But 5 per cent annually is as reasonable an estimate as any.

It's good to remember a couple of things before freaking out about that $8,000-plus estimate. Firstly, your salary will likely change over time – hopefully upwards – so you should be allocating more to your retirement fund as you get older. Additionally, it's unlikely that you'll be in a balanced account for the length of your working life.

Funds suggest that younger members start out in aggressive (high risk, higher return) products and move towards more conservative (low risk, lower return) products as they near retirement.

You should also consider the effect any embedded life insurance policies will have on your account balance.

Do we really need $1 million to retire comfortably?

Generally speaking, the goal in retirement savings and drawdown is to maintain your current lifestyle, plus or minus some expenses. This may include more expenses for travel, but less for commuting to work.

Many people focus on a number, such as a percentage of their regular pre-retirement salary. If you're eligible, the Age Pension will also provide some income in retirement.

Additionally, don't forget this important point: you do still have some earning power in retirement, especially if you maintain a modest allocation to income producing stocks in your portfolio. Some people overlook this.

Financial professionals often recommend basing your savings goal on your household's anticipated cash flow needs, rather than on an arbitrary number. The Retirement Standard set by the Association of Superannuation Funds of Australia (ASFA) suggests Australians will need less than $1 million to retire.

It estimates a super balance at retirement of $545,000 for an individual, and $640,000 for a couple, will "enable an older, healthy retiree to be involved in a broad range of leisure and recreational activities and to have a good standard of living".

This figure drops to $70,000 for both a single Australian and a couple if they're targeting a "modest retirement style". ASFA defines this as "better than the Age Pension, but still only able to afford fairly basic activities", indicating the above amount plus the rate of the Age Pension meets the need for this retirement style.

Both budgets assume retirees own their own home outright, are relatively healthy, draw down all their capital and receive a part Aged Pension.

The point is, it can be difficult but not impossible to save a considerable amount for your retirement. Especially if you afford to put away a little bit each month. Though for some it may be out of reach, for others it may be more achievable than they thought.

More in this series

• Investing basics: everything you need to know about reporting season

• Investing Basics: How do your savings compare to those of your peers?

This piece has been adapted from an article on Morningstar.com senior editor Karen Wallace.

Emma Rapaport is a reporter for Morningstar Australia.

Make better investment decisions with Morningstar Premium | Free 4-week trial

© 2018 Morningstar, Inc. All rights reserved. Neither Morningstar, its affiliates, nor the content providers guarantee the data or content contained herein to be accurate, complete or timely nor will they have any liability for its use or distribution. This information is to be used for personal, non-commercial purposes only. No reproduction is permitted without the prior written consent of Morningstar. Any general advice or 'class service' have been prepared by Morningstar Australasia Pty Ltd (ABN: 95 090 665 544, AFSL: 240892), or its Authorised Representatives, and/or Morningstar Research Ltd, subsidiaries of Morningstar, Inc, without reference to your objectives, financial situation or needs. Please refer to our Financial Services Guide (FSG) for more information at www.morningstar.com.au/s/fsg.pdf. Our publications, ratings and products should be viewed as an additional investment resource, not as your sole source of information. Past performance does not necessarily indicate a financial product's future performance. To obtain advice tailored to your situation, contact a licensed financial adviser. Some material is copyright and published under licence from ASX Operations Pty Ltd ACN 004 523 782 ("ASXO"). The article is current as at date of publication.