Hedging for currency risk

Currency movements can erode or boost returns. Here’s what to consider.

The Aussie dollar fell off a cliff at about 1.15pm New York time on Wednesday. Simultaneously, yields on US 10-year notes leapt like salmon up a waterfall.

The cause? The Federal Reserve’s June meeting, which revealed that rates could rise in 2023, earlier than expected. Investors responded by selling long-dated bonds.

The meeting set off a chain reaction in currency markets. Higher yields make US bonds more attractive for global investors, while higher inflation signals stronger growth.

Both can send the US dollar soaring says Steve Miller, an advisor at GSFM funds management.

“High bond yields widen the interest rate differential between the US and the rest of the world, so money flows from European bonds into US bonds,” he says.

“There is also a recovery dynamic because higher inflation is typically associated with stronger growth.”

So, all else equal, Aussies with US investments are richer today thanks to the Fed.

Events like this underscore how currency affects investment portfolios. Is currency hedging worth it for investors? How much does it cost? What should they keep in mind? We examine this and more below.

Currency risk

Currency hedging protects overseas investments from currency changes. Its increasing relevance for investors coincides with the growing popularity of international equity ETFs.

Imagine you buy a US dollar investment. You decide to sell. However, before you do, the US dollar falls in value. As a result, your investment is worth less when it is converted back to Australian dollars. Consider the following example:

On Monday Susie buys $1,000 of GameStop shares in the US through an Australian broker. With each Aussie dollar buying 0.75 US cents, she effectively owns US$750 worth of shares.

On Tuesday Elon Musk tweets a meme with the word “game” in it. GameStop increases by 10 per cent; Susie’s shares are now worth US$825.

On Wednesday, the Federal Reserve raises interest rates. Tens of billions flood the US hungry for higher rates. The US dollar surges as investors scramble into US funds; and the Aussie dollar falls, now buying 0.70 US cents.

On Thursday Susie’s had enough. She sells and receives $1178.5 after conversion. She owes $100 to Musk’s tweet, while the remaining $78.50 is thanks to a stronger US dollar.

Had the Aussie dollar instead risen to 0.80 US cents on Wednesday, Susie would be left with only $1031. Almost $70 of her return would have been eaten up by the foreign exchange markets.

And just like that, currency movements can erode or boost returns.

Impact of currency movements on repatriating US$55,000 worth of US equities to Australia

Hedging in practice

Investors have several options when it comes to hedging. Many Australian international equity ETFs have hedged and non-hedged versions.

These hedged ETFs use currency forward contracts to reduce their foreign-currency exposure, says Morningstar director of ETF research Ben Johnson.

A currency forward contract is an agreement between two parties to buy or sell a prespecified amount of a currency at some point in the future (typically one month out in the case of currency-hedged ETFs) at an exchange rate agreed upon between the two parties.

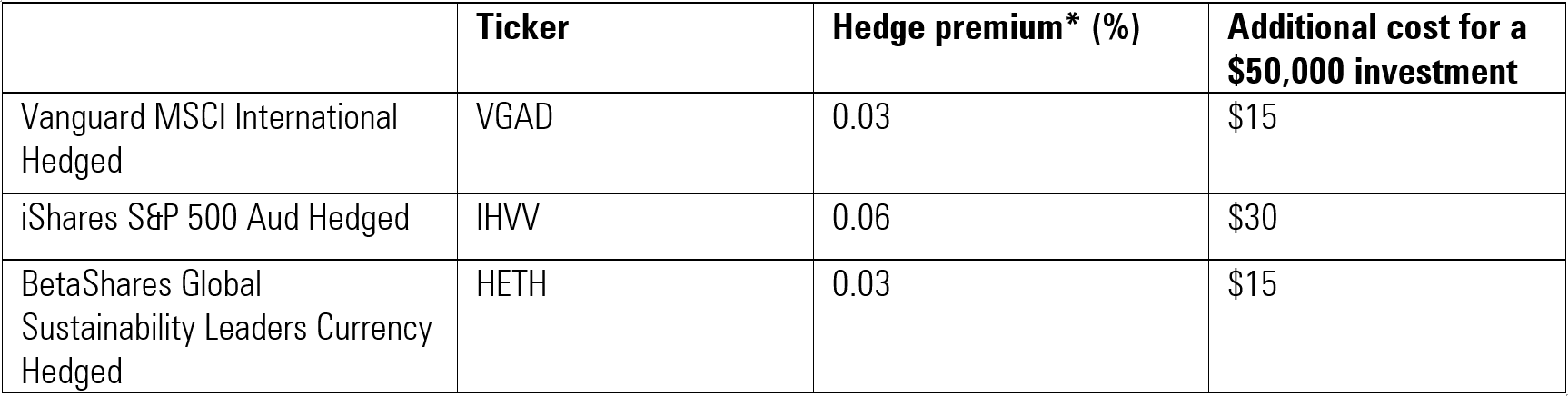

But these hedges come at a cost. Below are the “hedging premiums” of several large international equity ETFs.

ETF currency hedging premiums

Source: Morningstar Direct

*Management fee of hedged vs. non-hedged version.

Currency risk not all bad

For Australians, some currency risk can somewhat counterintuitively reduce the overall risk in a portfolio, says Tim Murphy, Morningstar director of manager research services.

In moments of crisis when global equity markets fall, such as during the GFC, investors look for safety, often in the US dollar.

Australia’s heavy commodity exposure makes it a relatively riskier area. So generally, during crises, the US dollar rises and the Aussie dollar falls.

For investors holding US equities, this movement can cushion a fall in the investments. An investor who held US equities that had fallen 10 per cent during the GFC could take some solace from the fact that a falling Aussie dollar meant their investments would be worth comparatively more when repatriated.

“The Aussie dollar is viewed globally as a commodity and ‘risk-on’ currency, so when you have a ‘risk-off’ event in markets, it has tended to sell off,” says Murphy.

“That happened in a big way in the Covid drawdown last year. The Aussie dollar went from buying about 70 US cents to around 55 in the space of a month. In the GFC the Aussie dollar went from about 90 cents to 65 over the course of 2008.”

Risk appetite

Currency hedging is a form of downside protection. Investors are protected against overseas investments falling in value because the Australian dollar rises; conversely, they lose the potential upside if the dollar falls.

Morningstar's model ETF portfolios global equity allocation are 45 per cent hedged.

Investors sure the Aussie dollar will fall want unhedged investments. Those sure it will rise, the opposite. The rest should consider partial hedging, says Murphy.

“In the short term, trying to take a view on currency movements, anyone who tells you they can do that is a liar,” he says.

“We think partial hedging is a sensible middle ground, because it dampens volatility along the way.”