3 things to know about thematic funds

From cannabis funds to artificial intelligence, investors have been piling into thematic investment options. Morningstar research shows where the money is going and why.

The global menu of thematic funds has ballooned in recent years as a growing number of funds attempt to harness secular growth themes, which can include everything from artificial intelligence to cannabis.

This steady supply of niche and often gimmicky funds from asset managers has increased demand from investors for clarity and guidance around this part of the market; investors need to be able to separate fad from theme.

To help meet this demand, Morningstar has developed a taxonomy for classifying such funds. Using this framework, we can analyse key trends in the market for thematic funds and help investors better navigate this landscape.

Here are three key takeaways from our recent study, which provides an overview of the global market for thematic funds.

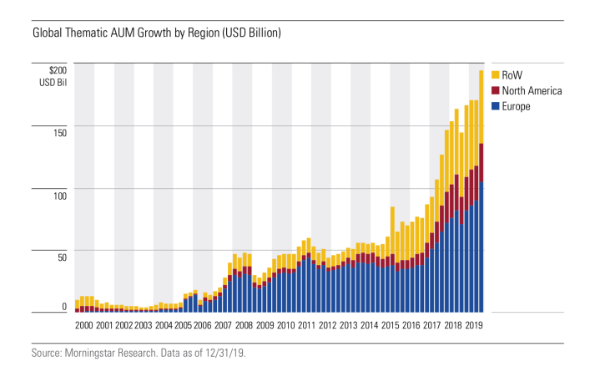

1. Assets in thematic funds have nearly tripled, and the menu is mushrooming

Investor interest in thematic funds is growing. Over the three years ended December 31, 2019, collective assets under management in thematic funds grew nearly threefold, from $75 billion to approximately $195 billion worldwide. This surge is shown in the chart below: Thematic funds now represent approximately 1 per cent of total global equity fund assets, up from 0.1 per cent 10 years ago.

Thematic funds now represent approximately 1 per cent of total global equity fund assets, up from 0.1 per cent 10 years ago.

The menu of thematic funds has also swelled. A total of 154 new thematic funds launched globally in 2019, falling just short of the record 169 new funds created in this universe in 2018. As of the end of December 2019, Morningstar’s global database was tracking a total of 923 thematic funds.

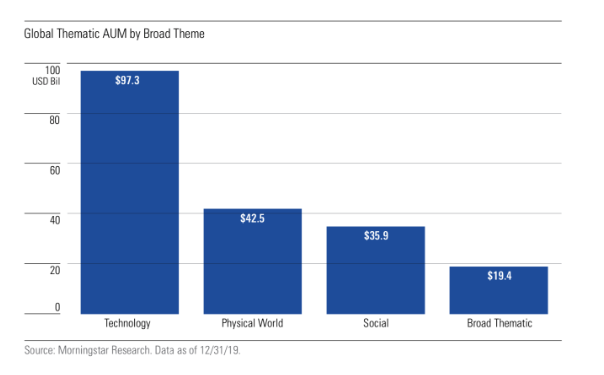

2. Thematic funds’ flows have been focused on a few themes

With $97 billion in assets as of the end of 2019, funds falling under the Technology Broad Theme in our taxonomy account for the majority of global thematic fund assets. The full distribution of assets across Broad Themes is shown in the chart below: Within that Broad Theme, funds fitting the Robotics and Automation theme held a combined $27 billion, making this the most popular theme globally. Investors flooded into these funds in recent years as performance within this segment surged. However, their appetite has more recently subsided following a stretch of more pedestrian performance.

Within that Broad Theme, funds fitting the Robotics and Automation theme held a combined $27 billion, making this the most popular theme globally. Investors flooded into these funds in recent years as performance within this segment surged. However, their appetite has more recently subsided following a stretch of more pedestrian performance.

This is just one of many examples of investors’ performance-chasing tendencies in the thematic fund space. The most prominent example was the rise and fall of Internet funds that coincided with the late ‘90s tech bubble.

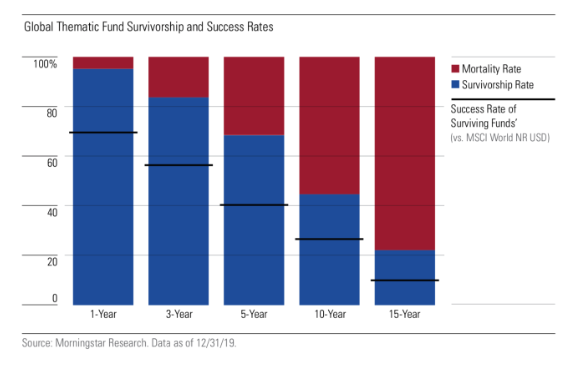

3. The odds are stacked against investors in thematic funds, but the prospective payouts are big

Investors in thematic funds are making a three-way bet. They are betting that they will:

- pick a winning theme,

- select a fund that is well-placed to harness that theme, and

- see valuations that indicate that the market hasn’t already priced-in the theme’s potential.

- The odds of winning these bets are low, but the prospective payouts can be large.

The long-term performance figures for thematic funds are pretty unflattering. As the chart below shows, just 45 per cent of all thematic funds launched prior to 2010 survived to 2020. Only a fourth managed to both survive and outperform the MSCI World Index over that 10-year span. That said, those that who do win, can win big. For example, those who invested in the ARK Next Generation Internet ETF back at the beginning of 2015 would have raked in annualised returns of 27 per cent through the end of 2019 - three times the return of the MSCI World Index over the same period. It’s performances like these that perpetuate these funds’ allure.

That said, those that who do win, can win big. For example, those who invested in the ARK Next Generation Internet ETF back at the beginning of 2015 would have raked in annualised returns of 27 per cent through the end of 2019 - three times the return of the MSCI World Index over the same period. It’s performances like these that perpetuate these funds’ allure.