Beleaguered Pact turning a corner

The specialist packaging group has again withheld a dividend but margins are improving and it’s putting the money to good use, says Morningstar’s Grant Slade.

Mentioned: Pact Group Holdings Ltd (PGH)

Narrow-moat Pact’s vital signs are beginning to turn a corner, despite weak packaging volumes which continued to challenge the core Australasian packaging segment in the first half of fiscal 2020.

Pact Group (ASX: PGH) will withhold a dividend for the second year running but will use the money to cut debt and pay for initiatives announced as part of its recent strategic review.

Morningstar analyst Grant Slade has cut his fair value estimate for Pact by 8 per cent to $3.60 a share after management flagged higher capital expenditure requirements over the fiscal 2020-fiscal 2024 period.

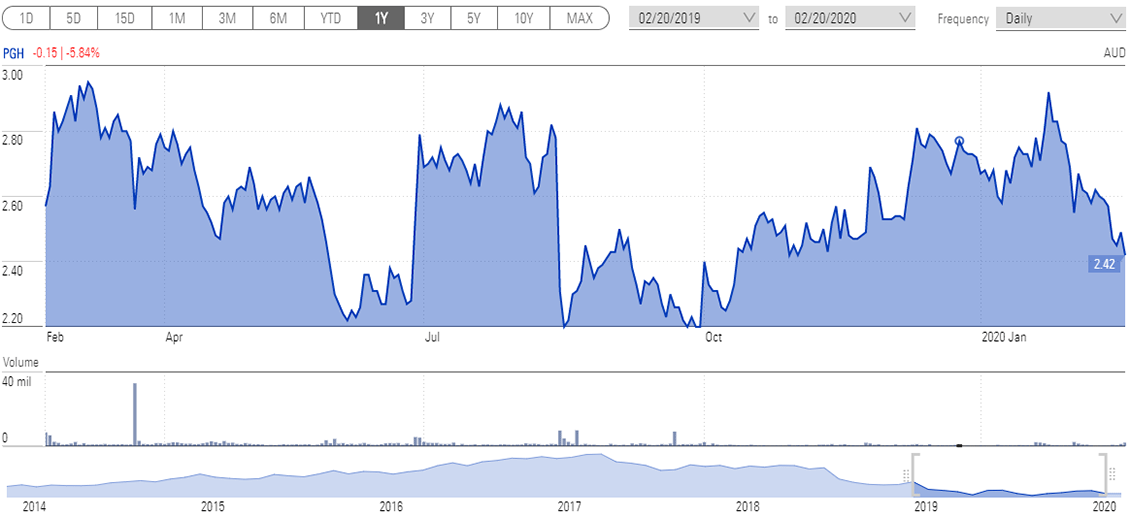

Pact remains significantly undervalued, trading at about a 30 per cent discount to Slade’s new fair value estimate. At 3.45pm on Friday, Pact was trading at $2.40.

The company is the largest rigid packaging plastics manufacturer in Australia and New Zealand. It makes packaging and containers for long-life products such as sauces, laundry detergents, and skin care products.

Source: Morningstar

It comprises a packaging segment, which accounts for about 65 per cent of operating income; a materials handling segment (this includes things such as milk crates for producers and accounts for about 27 per cent of operating income); and a contract manufacturing segment, which accounts for about 3 per cent and is currently up for sale.

Pact's underlying net profit for the half fell by 8 per cent to $32.7 million, from $35.7 million.

Excluding an accounting leases standard, net profit rose 4 per cent to $37 million.

Earnings at the packaging segment fell 1 per cent to $51 million amid challenging Australian volumes.

The company’s operating margin showed much needed improvement in the first half, Slade says, thanks to cost-cutting and a lower resin prices.

Its balance sheet troubles also eased because of the dividend suspension and cash flow generation.

Net debt fell to $667 million at 31 December 2019, reducing leverage to a more comfortable 2.9 times net debt/EBITDA.

Slade continues to forecast net debt/EBITDA of 2.9 times at fiscal 2020 year-end, which excludes the impact of the mooted contract manufacturing sale.

Some estimate this will go for $200 million, but Slade expects a more conservative figure of about $120 million. It will however inject “ample” cash into the balance sheet and allow the resumption of dividends.

“The divestment should allow for both major debt refinancing over the fiscal 2022--fiscal 2023 period to proceed and for the prompt resumption of dividends.”

Slade has downgraded his full-year fiscal 2020 EBITDA estimate by 2.5 per cent to $225 million as the company expects a slightly worse volume outcome in the core packaging segment.

The longer-term picture is brighter, he says.

“While near-term challenges for Pact’s business remain, our long-term expectations are unchanged and we continue to forecast a return to organic growth from fiscal 2021 onward.

“Long-term, we continue to expect population growth, rising per capita incomes in Australasia and Asia, and the pass-through of cost inflation to drive organic top-line growth of approximately 2.5 per cent,” Slade says.

Pact’s previously announced cost-cutting programme, in tandem with modest operating leverage, will see margins improve toward 9 per cent at midcycle, up from 7.6 per cent in fiscal 2019.