FAANG stocks after the market rout

Tech stocks took it on the chin on Thursday. Here’s our take on whether tech’s leaders are worth nibbling on.

Mentioned: Apple Inc (AAPL), Amazon.com Inc (AMZN), Meta Platforms Inc (META), Alphabet Inc (GOOG), Netflix Inc (NFLX)

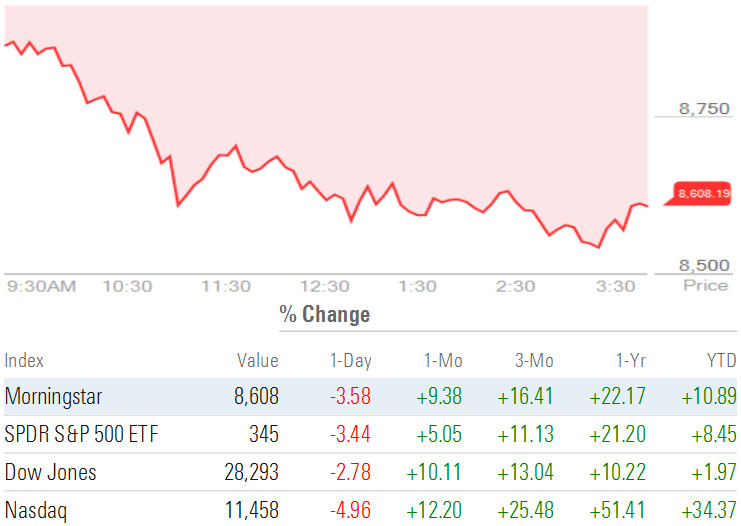

After a huge stretch of outperformance, technology stocks slid on Thursday, driving down the increasingly concentrated, tech-heavy S&P 500 by 3.5 per cent. Widely held FAANG stocks were knocked around, with Facebook (FB) off 3.8 per cent, Apple (AAPL) skidding more than 8 per cent, Amazon (AMZN) sliding 4.6 per cent Netflix (NFLX) down 4.9 per cent, and Alphabet Inc. (GOOGL) shedding more than 5 per cent.

Prior to yesterday, tech stocks had been on a tear: The Morningstar US Technology Index was up more than 40 per cent for the year to date, with most FAANG stocks returning more than that - led by Apple’s extraordinary 80 per cent year-to-date gain.

US Market | 1 day change

Source: Morningstar Direct

Whether Thursday’s sell-off is merely a speed bump for tech stocks or more than that is anyone's guess. Based on fundamentals, though, should investors buy the FAANG names on the dip - or on any further dips going forward?

As of Thursday’s close, none of the FAANG stocks is cheap - in particular, Apple and Netflix remain significantly overvalued by our standards. However, Facebook closed slightly above our fair value estimate, while Amazon and Alphabet both closed below fair value. All three stocks carry high uncertainty ratings; as such, we’d recommend investors wait for some margin of safety before diving in.

MORE ON THIS TOPIC: Pullback brings stocks closer to fair value

Here’s what our analysts had to say about each stock in their most recent Stock Analyst Notes.

Facebook (FB)

Fair Value Estimate: US$265.00

Thursday’s Close: US$291.12

Uncertainty: High

Economic Moat Rating: Wide

“Facebook reported second-quarter results above our projections and the FactSet consensus estimates as the firm continued to attract ad dollars even during the economic downturn. Users and their engagement on Facebook’s platforms continued to grow, displaying the resilience of the firm’s network effect moat source. Facebook remains the most attractive platform for what has become the most highly demanded ad type by advertisers, direct response, which has minimized the impact of lower brand ad spending. Regarding guidance, the firm does not expect revenue growth to accelerate in the third quarter as the end of various lockdowns and quarantines in different markets may lower user growth and engagement. Also, uncertainty surrounding the macroenvironment persists, and limitations on data usage could be imposed on the firm and its peers by lawmakers and companies such as Apple.

Due to the strong second-quarter numbers, we have increased our projections for this year and 2021 which resulted in a US$265 fair value estimate, up from US$245.”

Ali Mogharabi, senior analyst

Apple (AAPL)

Fair Value Estimate: US$71.00

Thursday’s Close: US$120.88

Uncertainty: High

Economic Moat Rating: Narrow

“While narrow-moat Apple remains well positioned in the near term given the upcoming 5G iPhone and stronger outlook for Mac and iPad segments due to the ongoing work- and learning-from-home dynamics, we recommend prospective investors wait for a wider margin of safety given the precarious state of the global economy, particularly as shares have appreciated more than 125 per cent from mid-March lows.”

Abhinav Davuluri, strategist

Amazon (AMZN)

Fair Value Estimate: US$3,500.00

Thursday’s Close: US$3,368.00

Uncertainty: High

Economic Moat Rating: Wide

The announcement of Amazon Halo - a healthcare monitoring subscription service--won't immediately move the needle on our valuation assumptions, but it joins Haven Healthcare (the healthcare joint venture between Amazon, Berkshire Hathaway, and J.P Morgan) and PillPack as another pillar to wide-moat Amazon's broader healthcare aspirations while giving us greater conviction in our longer-term cash flow assumptions.

There is no change to our US$3,500 fair value estimate--which assumes 22 per cent average annual revenue growth and operating margins approaching 10 per cent over the next five years - and we see shares as slightly undervalued.”

R.J. Hottovy, strategist

Netflix (NFLX)

Fair Value Estimate: US$200.00

Thursday’s Close: US$525.75

Uncertainty: Very High

Economic Moat Rating: Narrow

“Netflix posted a second straight quarter with impressive subscriber growth as people continue to demand entertainment options at home during the COVID-19 pandemic. Despite subscriber additions coming well ahead our estimate and guidance, revenue was in line with our projections for the quarter. We still view much of the subscriber beat as a pull-forward of longer-term growth and expect the global rollout of Disney+ and the recent launches of Peacock and HBO Max to increase churn. However, we are raising our FVE to US$200 from US$160 to account for the revenue impact of the larger subscriber base and slightly faster margin expansion than previously expected.”

Neil Macker, senior analyst

Alphabet Inc. (GOOGL)

Fair Value Estimate: US$1,690.00

Thursday’s Close: US$1,641.84

Uncertainty: High

Economic Moat Rating: Wide

“Strong performances by Alphabet’s YouTube, cloud, and Google Play helped partially offset a decline in search ad revenue and resulted in second-quarter numbers above our expectations and the FactSet consensus. The firm has begun to see slight month-over-month improvement in search ad spending, although the business remains heavily dependent on an economic recovery. We continue to expect slight improvement in Google’s total ad revenue during the remainder of 2020 as the decline in search slows a bit and demand for direct-response ads continue to increase for YouTube. Google’s other segment is likely to continue to grow strongly this year, further diversifying Alphabet’s total revenue. Given the better-than-expected top- and bottom-line results in the second quarter and our assumption that Google will successfully monetize some of its other properties in the long run, we have increased our projections, resulting in a US$1,690 fair value estimate, up from US$1,520. This wide-moat and high-uncertainty name appears fairly valued, but we would not hesitate to accumulate shares during a pullback.”

Ali Mogharabi, senior analyst