Morningstar: Xero still expensive despite fair value upgrade

International expansion has yet to gain traction for the accounting software provider.

Morningstar has slightly increased its fair value estimate for Xero despite weaker than expected full-year earnings results and slowing international expansion.

While the full-year results were lower than expected, the longer-term outlook has not materially changed, according to Morningstar equity analyst Gareth James. His upgrade reflected slightly higher long-term earnings forecasts.

The main challenge continues to be breaking into the lucrative but competitive US market, says James.

“Xero's failure to capture material market share from incumbent provider and industry giant Intuit means competition will likely remain strong in other key markets, such as the UK.”

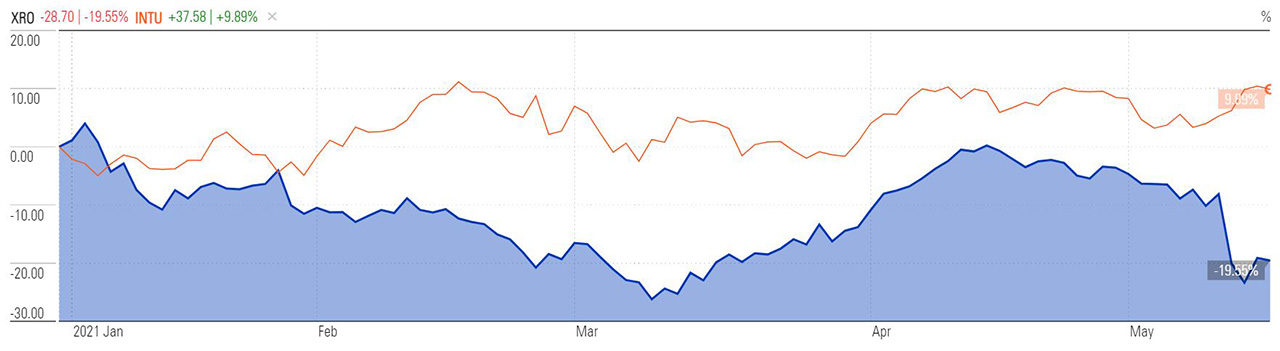

The fair value estimate was upgraded on Monday by 9 per cent to $50. Narrow-moat Xero (ASX: XRO) closed Tuesday at $117.32, a 135 per cent premium on the fair value estimate. The firm has a price / earnings ratio of 555.56.

Its wide-moat US competitor Intuit (INTU) closed US$417.43, a 33 per cent premium on the FVE of US$310.

Shares in Xero fell 13 per cent last Thursday on a disappointing full-year earnings report. The company reported a 1 per cent fall in average revenue per user and downgraded earnings guidance for fiscal 2022.

The revenue decline was concentrated in the important international business, where it fell 3 per cent.

James says last Thursday’s drop was excessive and that Xero got caught up in broader market fears over how higher inflation would affect growth stocks.

“Several ASX-listed growth stocks, which performed well in 2020, have experienced significant share price weakness in recent weeks,” he says.

“Weak earnings announcements have combined with higher interest rate expectations to reverse previously strong share price momentum.”

Yields on US 10-year Treasury bonds, which tend to rise when investors expect rising inflation, rose 90 per cent from 0.917 per cent in January to a peak of 1.745 per cent at the end of March. They closed Tuesday at 1.64 per cent.

Higher inflation expectations imply higher interest rates which have a disproportionately negative impact on high growth stocks.

James’s report also notes how the push to keep up the growth of new subscriptions came at the cost of quality, with subscription growth outpaced revenue growth, 20 per cent to 18 per cent. James believes investor pressure means this is likely to continue.

Full-year earnings before interest and taxes (EBIT) rose 96 per cent to NZ$62 million thanks to a strong first half. Second half EBIT was negative NZ$1 million.

The consensus analyst forecast for Xero is “outperform”, according to Pitchbook data. There are six buy calls, five holds, and four sells, as of 19 May.

Xero and Intuit share price change (YTD)

International competition remains a hurdle

Xero’s priority has long been subscriber growth and international expansion, but competition is much fiercer in the important US market, says James.

The firm reported higher monthly churn in its international business compared to what the ANZ business achieved at a similar stage previously. Churn measures how much revenue is generated by subscribers who quit the product in a month.

Subscriber growth in the US also fell versus the previous year, from 24 per cent to 18 per cent. Revenue growth was also disappointing, with a 6 per cent increase in US operating revenue on constant currency basis.

Concerns about overseas expansion were also echoed by ST Wong, CIO of Prime Value Asset Management.

"Xero's growth and business model are quite attractive,” says Wong.

“The downside is that its expansion into the US, which the company has tried multiple times, has yet to gain traction.”

Last week’s results are broadly in line with Morningstar’s long-term view, says James.

“Xero will continue to prioritise subscriber growth over profits but will experience a tougher competitive environment overseas than in Australia and New Zealand, or ANZ.”