Opportunity in Challenger despite earnings tumble

The annuity provider has felt the pain of covid-19 market volatility as investment yields on its defensive assets fall.

Challenger's chief executive Richard Howes delivered a blow to investors on Tuesday. After a strong first-half fiscal 2020 result, the retirement income specialist announced a 13 per cent profit plunge amid weak sales and declining investment returns.

Normalised net profit after tax fell 13 per cent from the prior year to $344 million, marginally below Morningstar's forecasts. Morningstar equity analyst Shaun Ler said this was largely thanks to lower investment yields from defensive assets, as the covid-19 pandemic economic turmoil ripped through global markets.

Major structural change in the financial advice industry also weighed on Challenger's local annuity sales. This includes the exit of major banks from aligned advice in the aftermath of the banking royal commission and independent financial advisers coming to the forefront.

But it wasn't all bad news for Challenger (ASX: CGF). Strong performance fee growth from its boutique asset management firm Fidante partially offset drawbacks, Ler says. Fidante partners with several investment management firms including Greencap Capital, WaveStone Capital, Kapstream and Alphinity.

Howes drew investors' attention to growing funds under management, up 4 per cent to $85 billion, and growing life sales, up 13 per cent thanks to sales in international markets.

"This result in very challenging conditions demonstrates the benefits of our strategy to diversify our products and distributions channels," he said in an ASX release.

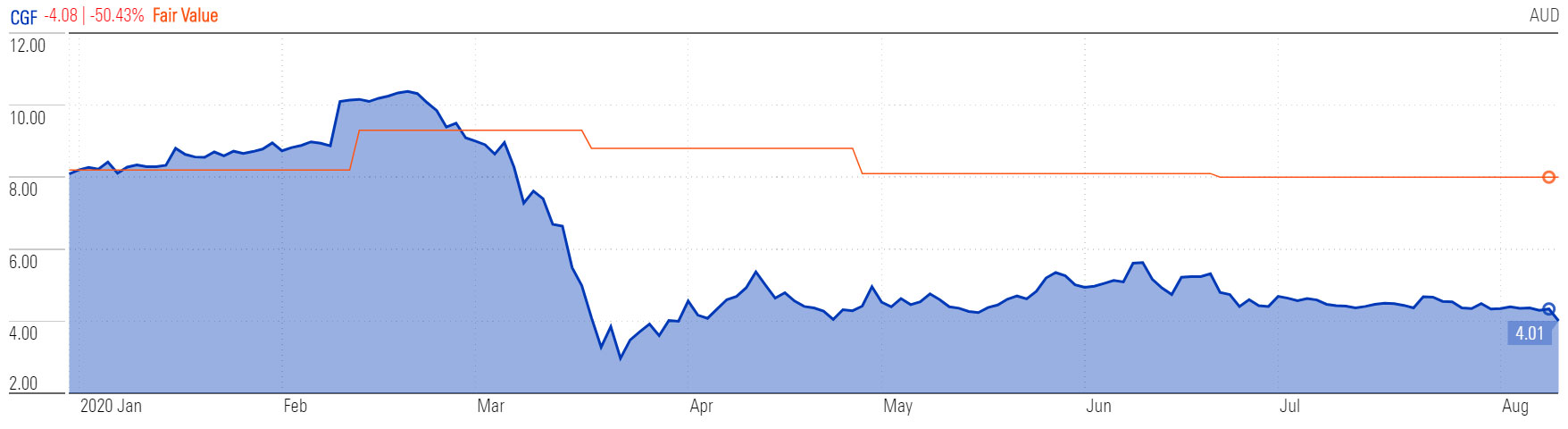

Ler cut his fair value estimate for Challenger from $8 to $7.20 following the earnings release. At Tuesday’s $4.01 close, shares are significantly undervalued, trading at a 50 per cent discount.

See Ler's full research note:  Near-Term Challenges Weigh on Challenger, but We Believe the Growth Story Is Intact

Near-Term Challenges Weigh on Challenger, but We Believe the Growth Story Is Intact

Challenger (ASX: CGF) | Price to fair value, YTD

Source: Morningstar Premium

‘Green shoots’

Ler sees signs of life in businesses long-term growth strategy. "Green shoots" are emerging, he says, from Challenger's strategy to "diversify its distribution channels, develop new products, and sell longer-tenured annuities".

"Starting fiscal 2022, we forecast a pick-up in annuity sales growth, reduced maturity rates, and a more aggressive asset allocation to support higher future returns," Ler says.

"We believe Challenger can navigate through the current disruptions to the financial advice industry and low rate environment and continue growing annuity sales."

Ler expects total annuity sales to grow around 10 per cent per year to fiscal 2025, backed by:

- "an ageing demographic

- increased compulsory super contributions

- ongoing annuity sales into Japan, and

- the proposed new covenant requiring super funds offer a retirement income product by July 1, 2022."

He says Challenger's new annuity linked to the RBA cash rate "should also appeal to investors who held off buying annuities because of low rates".

Ler also believes Challenger can expand its distribution and leverage institutional and overseas demand for its products.

"The move to partner with more non-major bank and independent financial advisers is bearing fruit, with this channel contributing close to 90 per cent of sales of new lifetime annuities, which should receive more take-up under the new age pension means test," he says.

Shrinking margins

There will be some challenges, however, in the company's growth strategy. Ler says margins are likely to be lower in the future as Challenger partners with large industry superannuation funds.

"Superfunds typically have strong bargaining power, which allows them to demand higher annuity yields," he says.

He also warns that Challenger is susceptible to competition, either from incumbent Australian or large international life insurers.

On the funds management side, Ler says the business has some vulnerability – namely to superfunds internalising asset management and disruptions in the financial advice industry.

In the near term, Ler anticipates soft near-term annuity sales, higher maturity rates, lower investment yields and higher operating costs.

The company failed to pay a financial year dividend but Ler forecasts an increase in dividends from fiscal-2021.

Stewardship rating downgrade

Ler has now downgraded Challenger's stewardship rating – a measure of capital allocation decisions – from Exemplary to Standard.

"Despite management's sensible capital allocation, excess returns have eroded over time with returns on equity (post-tax) falling to 10 per cent in fiscal 2020, from 16.1 per cent in fiscal 2014," he says.

"We think Challenger faces the tough reality of not being able to invest considerably into high-returning assets, as well as the commodification of its products and having to operate in a low-barriers-to-entry industry."

Challenger was among a handful of ASX-listed businesses which carried the Exemplary stewardship rating. Macquarie Group (ASX: MQG) is now the only financial services company in this category.

Morningstar's stewardship rating is an assessment of how a company’s managers behave on behalf of shareholders. In short, how management uses the money/capital they have at their disposal to create value for shareholders - the owners of the company.

MORE IN THIS TOPIC: The Morningstar Four: How to spot a well-managed company

This article is part of Morningstar's Reporting Season 2020 coverage. The calendar will be updated daily to connect you with our equity analysts' take on the financial results.