Unibail fair value slashed amid uncertain future

Unibail-Rodamco-Westfield had a tough first half. Its second half is expected to be worse.

Mentioned: Unibail-Rodamco-Westfield (URW)

If there's one industry that has been hit with the full force of COVID-19 restrictions it’s retail property. And its future is looking no less uncertain even as countries end lockdowns.

Unibail-Rodamco-Westfield (ASX: URW), Europe's largest listed commercial property operator with a portfolio of shopping centres, offices and convention centres, was devastated by continent-wide lockdowns and a fall in foot traffic, forcing most of its retail tenants to shut up shop. Bans on large gatherings also infected its events business.

Morningstar director of equity research Adam Fleck says the company's first-half earnings could have been a lot worse considering what they were up against. Statutory earnings were down roughly 30 per cent on the first half of 2019. But Fleck says the situation will likely deteriorate as the full impact of the pandemic is revealed.

"Statutory earnings for the half were not disastrous; however, we expect the annual result will be worse," Fleck says.

"This seems counterintuitive because the worst of the shutdowns were in the second quarter, with most centres reopened by June, but the statutory accounts will take time to reflect the damage."

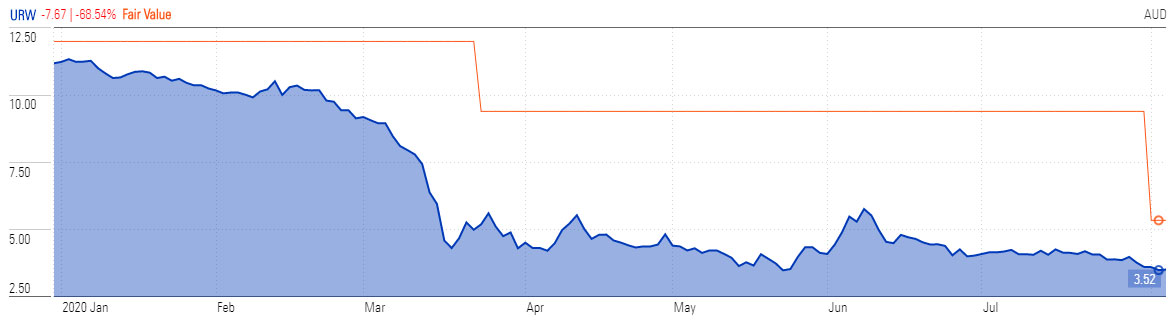

Reduced rent expectations from Unibail's retail properties and lower expected earnings from the office and convention divisions have led Morningstar to dramatically reduce the group's fair value estimate by 30 per cent.

This reduction – to €65.30 ($5.35) from €101.50 ($9.40) – follows a similar move by analysts in March when Unibail's survival was questioned.

Unibail's uncertain future is characterised by several unknowns.

First, the group is only a quarter of the way through renegotiating rent with its tenants. Where waivers are agreed to, Fleck explains that accounting standards require the discount to be "straight lined", meaning that it will be recognised over the life of the lease term, not the month in which the discount applies.

"Based on rent reductions agreed so far, the cash impact has been €32.6 million ($54 million), but the impact on the profit and loss statement (P&L) was only €15.6 million," he says.

"That timing difference will eventually flow to the P&L, plus the effect of future negotiations, plus tenants that default, and there will be effects on leasing of new space."

The ability of tenants to meet deferred rental payments is also a "substantial unknown". Unibail granted rent deferrals to most of its tenants amid the enforced shutdowns in the second quarter. However, Fleck says it is unclear whether those tenants will be able to make those payments when they come due.

"Deferrals mean provisions for doubtful debts that will likely eventuate, have not yet been recognised in the accounts—in other words, a tenant can't default if the rent isn't due.

"Half of overdue rent is recognised as a doubtful debt only 90 days after the due date, and the other half is recognised once it is 180 days late."

Capital raise unlikely

Morningstar's base case is that the company will avoid an equity raise. Unibail issued more than €2 billion in bonds in April and June and has more than €12 billion of cash or undrawn credit lines. Fleck believes the company could also further reduce development capital expenditure if pressure mounts, which will give them several years of reprieve.

URW is currently trading at discount to its fair value estimate, despite the steep FVE reduction. However, the stocks "very high" uncertainty rating and volatile trading in late-May and early June should however be a warning to investors to tread cautiously.

"Any impact on earnings or asset prices, which are important at the moment given Unibail's planned asset sales, has a substantial effect on our fair value estimate," Fleck says.

Unibail withdrew its earnings guidance and did not provide full-year guidance at the half-year result.

Unibail-Rodamco-Westfield FVE movements, YTD (ASX: URW)

Source: Morningstar Premium

Shifting foundations

Fleck believes shoppers will return once the virus fears fade. This should lead to rebounds in rent collections, particularly where long-term leases can be enforced. And there are some encouraging numbers.

"Unibail said that in the centres that had reopened for 11-12 weeks, footfall has recovered to 80 per cent to 90 per cent of normal levels," he says.

"Average sales baskets were actually higher, probably because shoppers visited for specific higher value purchases, rather than food, and did not linger."

But none of this is certain. The longer the crisis drags on, the more likely it is rents will fall.

"The longer the COVID-19 crisis lingers, the more of a rebasing downward effect is likely for future rent," Fleck says.

"This effect will be most pronounced in newly rented space, which is substantial for Unibail given its development pipeline."

Long-term uncertainties include how willing consumers will be to re-enter public spaces, lingering economic effects once the virus abates and the risk that a temporary switch to online portals turns into permanent changes in consumer behaviour.

This article is part of Morningstar's Reporting Season 2020 coverage. The calendar will be updated daily to connect you with our equity analysts' take on the financial results.