Will this be the year active ETFs succeed?

Active managers are poised to grab a bigger piece of the $80bn exchange-traded pie but hurdles remain.

A perfect storm is brewing for active managers. Magellan's transformation of its three global equity funds into a single unit structure, accessible on and off the ASX, simplified the process of bringing an unlisted fund to the exchange. Meanwhile, ASIC's lifting of its six-month suspension of non-transparent actively managed ETFs removed uncertainty surrounding the use of internal market makers. This has cleared the way for active managers to grab a bigger piece of the $80 billion ETF pie.

"This new listed/unlisted structure will see a wave of managers looking to list actively managed products," Chi-X director, product, sales and data, Shane Miller says.

"For a manager, it's just a simpler process to add exchange distribution rather than duplicating everything. Plus, they get to leverage their fund's existing ratings and performance history."

Magellan's restructure of its global fund last year from an open-end fund, an ETF and a closed-end fund into two classes of units; an open-end (MGOC) and a closed-end fund, brought a new find of active ETF to the exchange. It essentially combines the feature of a traditional unlisted managed fund and an active ETF. Previously managers were forced to create a copy of their existing fund for the purpose of listing.

Miller expects an incredible 30 ETFs will be quoted on Chi-X by mid-2021, adding to the 11 trading today. "The majority of those listing to come are actively managed ETFs," he says. As the junior rival, Chi-X’s activity gives you an idea of what could be happening at the ASX.

"We've taken a lot of phone calls from managers who are looking to add exchange distribution to their existing products," Chi-X head of product development Ross Pullen says.

"They're looking at how much is flowing into passive ETFs and thinking there's a whole distribution area we're not accessing – particularly SMSFs."

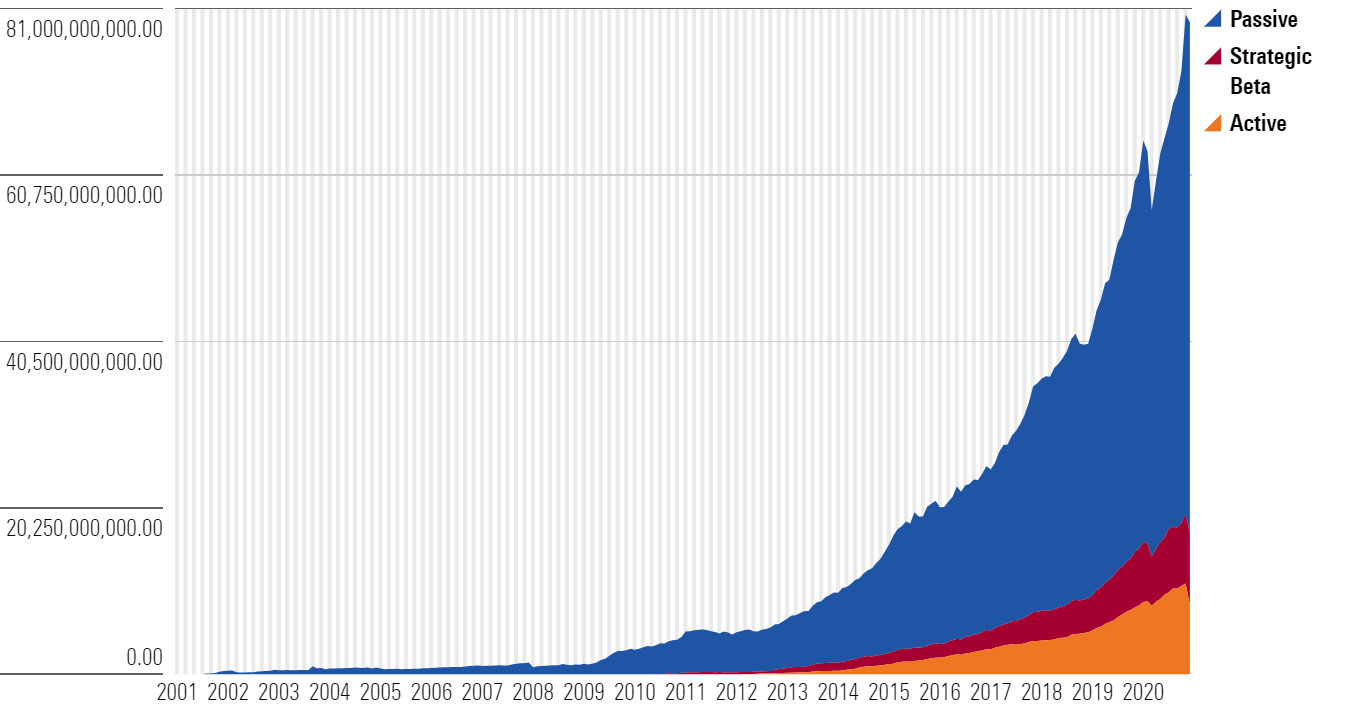

Active ETFs are still a small piece of the Australian ETF industry

Source: Morningstar Direct

Active ETFs aren't new to the Australian market, but most product providers have failed to attract significant attention. In 2020, passive products pulled in over $17 billion to active's $2 billion. Retail investors are far more likely to use passive ETFs to build their portfolios citing historic underperformance, fees and simplicity.

Active ETFs combine the benefits of active fund management with the convenience of share trading. They are managed by a team of portfolio managers who make decisions on the underlying portfolio allocation and aim to outperform an index or benchmark.

Chris Meyer, director, listed products at Pinnacle Investment, cites several reasons for underwhelming flows, including a lack of branding, marketing and awareness for retail investors, and the industries' inability to break into the advice/broker market.

Retail assets in Australian unlisted funds have grown steady over the last decade thanks in part to strong relationships between managers and the advice community, but it's clear firms can see the train coming. In the US, the scale has tipped in the opposite direction, with investors accessing more listed products than unlisted in 2020. ETFs took in a record $502 billion in 2020, while investors pulled $289 billion from open-end mutual funds, Morningstar data shows. While mutual funds total assets still dwarf those in ETFs, Morningstar's John Rekenthaler believes ETFs are positioned to take over.

"ETFs offer several advantages that managed funds cannot match," he says. "Eventually, assets will be on their side."

The wild success of the ARK Innovation ETF in the US also shows the market for active products is there. But there are other good reasons for managers to diversify their distribution strategy, chief among them the shifting advice landscape.

Ark's red-hot actively-managed ETF is one of the fastest growing funds in the US

.jpg)

ARK Innovation ETF (ARKK) estimated flows and returns. Source: Morningstar Direct

"Advisers are looking for ways to simplify the business operations, with some moving towards separately managed accounts," he says referring to a professionally managed investment product where investors directly own the underlying securities (rather than having their funds pooled with other investors).

"Listed products fit quite nicely inside managed accounts. As that trend takes hold, I think it stands to reason that listed funds inside these SMAs will gain more traction."

Secondary reasons include access to a wider market and future proofing. Several roadblocks have locked unadvised retail investors out of the unlisted fund market, including high minimum entry amounts, long hand-written application forms and a general industry lack of interest in retail communication. Some managers have got it right. Magellan packed a convention centre in Sydney last year with retail investors, all of whom walked out with a promotional umbrella. The manager pioneered active ETFs in Australia.

New faces

So, who will be the next to list? Boutique growth manager Hyperion Asset Management will expand the footprint of its top performing global equity fund with an actively listed version on the ASX next month. Portfolio managers Mark Arnold and Jason Orthman say the product was born off the back of strong demand from advisers who are "wanting more and more listed products" and brokers. The new Magellan-style structure also appealed.

"The drumbeat has just gotten louder and louder to list, particularly from advisers" Orthman says. "And this new structure means we can have an quoted version of the same fund. You can inherit all the same research ratings, platforms, performance track record and unit prices. Plus, the fund already has over $1 billion in it, so fund size isn't a worry."

New research by Morningstar's Matthew Wilkinson shows some, particularly smaller ETFs, have run into considerable liquidity problems during times of extreme market volatility, as was seen in March 2020. Investors faced wide spreads, very thin market depth and instances of no bids or offers.

Meyer says the option of listing an existing fund, which carries the same analysts’ rating, shouldn't be underestimated. "Funds, whether they're listed or unlisted, still need good research ratings, still need to be in the approved product lists of advisers and brokers, and therefore still need a good track record. It's not like listed funds is a magic silver bullet for access to new capital."

Arnold and Orthman say they're hoping the listed structure will appeal to both advisers and retail investors who prefer listed funds. "That's a segment of the market we haven’t been able to access historically," Arnold says.

The listing comes after a strong decade for the fund, outperforming the MSCI World Ex Australia NR index over the 1, 3, and 5-year period. Stock picking success across the firm's three funds has helped it double funds under management, from $1.71 billion in 2019 to $3.5 billion today.

But Hyperion is just the beginning. Asset-class diversification is coming too. Miller says the 30 ETFs he anticipates will list on Chi-X will represent a range of asset classes including fixed income, Australian equity, international equities and liquid alternatives.

Meyer expects a lot of the action will be among fixed-income and global equity issuers due to the concentration of investor portfolios in Australian equities and the difficulty in accessing those asset classes.

The exchanges added 10 active products in 2020, including five from Magellan. Other issuers include Fidelity Australia, Antipodes, Intelligent Investor, K2, eInvest, Montgomery, Schroders and Platinum.

Active listings have grown since 2015

.jpg)

Number of ETFs listing on Australian exchanges, by year. Source: Morningstar Direct

If we build it, will they come?

There are thousands of unlisted funds domiciled in Australia. Does this mean the floodgates will open? Unlikely. While interest is increasing, there are still several hurdles.

It's one thing to list a product. It's another to attract flows. Meyer says he believes managers will seek to establish a name for themselves in the unlisted world first before using the exchange.

"We advised Hyperion to wait for strong performance and inflows in their unlisted fund before they listed," he says. "I believe the formula for a successful ETF listing should happen off the back of a successful unlisted managed fund, and not the other way around. At least until there is a wholesale move by advisers off platforms and onto the exchange."

Miller agrees, saying issuers will begin by tapping into their existing relationships with full-service brokers and platforms, before building out a brand marketing campaign for direct investors.

"If no one knows to look for your product, it's not going to sell," he says. "If you've got a brand name, we can offer a mechanism to access it, but that just listing isn't enough in itself to draw in investors."

Setting up an active product is also easier said than done. Issuers must meet exchange criteria, link with a market maker, build out an internal infrastructure etc. Miller says, however, that once managers go through the complexity of listing one fund, it's easier to list a second, and so on.

Morningstar senior analyst Christopher Franz has questioned whether the same research house ratings will flow between distribution models. He says at Morningstar, active ETFs are rated the same as open-end funds from an operational standpoint, meaning an analyst could adjust their view of a fund based on possible risks or difference in fee level.

Analysts have long warned about the pitfalls of trading less-liquid ETFs particularly on volatile trading days. Platinum's Asia fund (unlisted) and Asia ETF PAXX (listed) held two different ratings, gold the former, silver the latter, due in part to trading costs and wide spreads during periods of market volatility.

The active management industry will also need to repair its relationship with retail investors, and frankly, in many cases, introduce themselves. Former Morningstar senior analyst Andrew Miles says retail investors are within their rights to question the value of global equity active management, in particular, after decades of underperformance.

Investors can be forgiven for their disbelief. Issuers have trotted out the same message for the past few years – this is the year for active ETFs, everything is just right. But whether they take-off this year or the next, increased activity signals that exchanges are continuing to democratise access to investment products. Active joining the party will only amplify that trend.