Big four's $50bn capital raising spells investor opportunity

New bank capital regulations being rolled out locally over the next few years could open the door to a class of high-yielding bonds formerly only available to institutions, writes Arian Neiron.

Mentioned: VanEck Australian Sbdntd Dbt ETF (SUBD)

New bank capital regulations being rolled out locally over the next few years could open the door to a class of high-yielding bonds formerly only available to institutions, writes Arian Neiron.

Although it’s been more than a decade, the fallout from the global financial crisis is still impacting banks in the way they raise and hold capital.

The Australian Prudential Regulatory Authority has required banks and many financial institutions to hold more capital on their balance sheets since the GFC, when many large global financial institutions had to be bailed out using billions of taxpayer dollars. Governments and central banks worldwide do not want a costly repeat.

In response, the Bank of International Settlements’ Basel Committee boosted universal banking standards, requiring banks to hold more capital to reduce the likelihood of bail-outs.

Basel III and Tier 2 Capital

The latest iteration of these changes is known as Basel III. With an implementation deadline of 2019, this requires banks to issue an additional layer of bonds that convert into equity capital if an institution’s debt capital reserves are depleted.

Tier 2 Capital is an example of such debt. This is supplementary capital held by banks, composed of items such as revaluation reserves, hybrids and subordinated term debt.

Good news for investors

APRA, which implements Basel guidelines locally, issued new rules in July requiring banks to double the amount of Tier 2 Capital they hold. It is estimated that Australia’s big four banks will need to raise a combined $50 billion of Tier 2 Capital over the next four years to meet APRA’s demands.

This will create a much bigger market for subordinated debt. Up until recently, Australia’s financial institutions had issued only modest amounts of Tier 2 Capital.

That’s good news for investors. With the Reserve Bank of Australia cutting rates for the third time this year, retirees, who are generally more interested in income than in growth, are finding their investment choices limited.

Term deposits and Australian corporate and government bonds no longer provide enough yield. Subordinated debt provides a new way to fill the income gap.

The yield to maturity on the benchmark iBoxx AUD Investment Grade Subordinated Debt Index was 2.4 per cent as at 30 September, much higher than the 1.3 per cent average interest rate on 12-month bank term deposits at the same date.

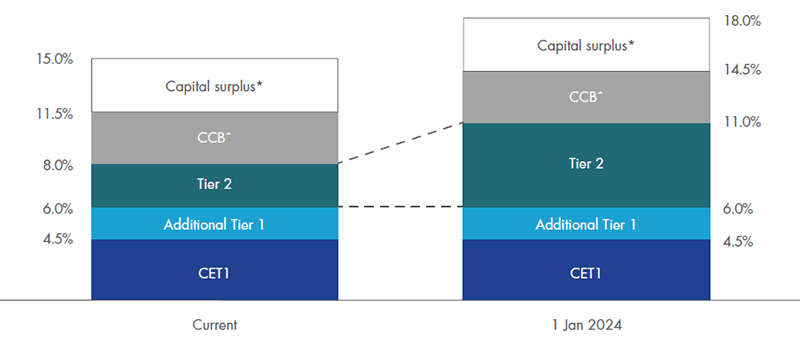

Tier 2 Capital to rise in importance

Tier 2 Capital will become more important as APRA is now requiring Australia’s big four banks to hold a lot more of it. As the chart below shows, subordinated debt from these financial institutions alone is expected to grow to 11 per cent from 8 per cent of risk-weighted assets over the next four years.

Changes to major banks’ capital structures

Source: ANZ Bank

The investor appeal of subordinated debt

With so much more subordinated debt to hit the market, it’s important to understand what it is.

Subordinated debt shares two basic characteristics with traditional bonds:

- It delivers reliable income

- An investor’s capital is relatively safe - in this case, because it is predominantly issued by the four largest Australian banks.

The following chart provides a simplified example of the capital structure in a financial institution to illustrate how different securities issued by banks rank in priority of payment in the event of insolvency.

Simplified capital structure of a financial institution

Source: ASIC

As the chart shows, priority is given to holders of deposits and other senior debt, while subordinated debt holders rank above ordinary shareholders and investors in Additional Tier 1 Capital – more commonly known as "hybrids".

For this reason, subordinated bonds are considered riskier than deposits or senior debt, but are less risky than shares and other hybrids. But the trade-off for this slightly higher risk is their generally higher interest rate versus other categories in the capital structure.

Subordinated debt is more debt-like than hybrids. Generally, interest payments must be met and funds repaid at maturity while the issuing financial institution is solvent.

However, in times of financial stress, interest payments on subordinated debt securities may be stopped indefinitely and they can be converted to equity or written off without the bank becoming insolvent or failing. This is because the purpose of Tier 2 Capital is as a fail-safe against costly taxpayer-funded bail outs, because it can be absorbed to prevent the failure of a bank.

The investment opportunity

Until now, subordinated debt has only really been available to large institutions. Now, investors of all sizes can access an investment grade subordinated debt portfolio.

Based on the roll-out of APRA's new Tier 2 Capital requirements, as outlined above, we believe the subordinated bond market is poised for significant growth.

Exchange-traded funds are one way investors can get exposure to this opportunity, including VanEck Vectors Australian Subordinated Debt ETF (ASX: SUBD). Though it isn't currently part of Morningstar's manager research coverage, this ETF features a portfolio of investment grade subordinated bonds.

SUBD tracks the iBoxx AUD Investment Grade Subordinated Debt Index, which only includes investment grade Australian currency floating rate bonds issued by financial institutions that qualify as Tier 2 Capital under APRA’s rules.

The index yielded around 2.4 per cent annually as at 30 September 2019. SUBD is another exchange traded fund opportunity that can assist in building investors’ income portfolio.

Investors should always read the product disclosure statement and consider obtaining financial advice before making an investment decision.