Cash rate tipped to sit around 2 per cent longer term

Disinflationary forces likely to keep inflation and the cash rate low longer term, say asset managers.

Investors are set for a brief “inflation hump” over the next year but it’s likely to be temporary as the forces that have kept inflation low since the GFC reemerge.

That was the view from senior fund managers at PIMCO and Macquarie Group, speaking at Morningstar’s Investment Conference on Wednesday and Thursday this week.

A combination of higher debt, lower population growth, and pressure on labour from weak bargaining power and digitisation are likely to act as “headwinds to global growth and inflation” in the post-covid world, according to Matthew Mulcahy, who heads Macquarie Investment Management’s global rates and currency fixed Income team.

There will be an adjustment period of higher inflation as economies reopen and companies adjust to the surge in demand but “pretty quickly” cyclical forces like rising commodity prices will pass.

“Structural forces ultimately dominate given that global growth really comes down to productivity and population growth,” said Mulcahy on Thursday.

“If you’ve got an aging population and a lack of productivity, you’re going to struggle to get global growth going.”

Mulcahy forecast a long-term “neutral” cash rate of around 1 per cent, with the headwinds having only grown since covid because of increases in debt and the shift to remote working thanks to digitisation.

Jay Sivapalan, head of fixed interest at Janus Henderson, was more optimistic and forecast a longer-term rate somewhere between 1.5 and 2 per cent, thanks to continuing stimulus, greater female workforce participation and migration.

The long-term cash rate, usually called the neutral rate of interest, is the theoretical rate that would prevail in an economy with full employment and stable inflation, a level where policy is neither expanding nor contracting the economy. The actual cash rate would fluctuate around it depending on the stage of the economic cycle.

The “big question” of the future of inflation was discussed across both days of the annual Morningstar Investment Conference.

Speaking on Wednesday, chief investment officer at bond manager PIMCO, Dan Ivascyn, thought inflation in Australia could peak as high as 3 per cent in the short term, but “disinflationary pressures” in the global economy meant it was likely to be a “headfake” and prove transitory.

“People that have been betting on an uptick in inflation, and a reversion back to more normal interest rates have been disappointed time and time again,” Ivascyn said.

Inflation fears have rattled markets recently. The US personal consumption expenditure index, favoured by the Federal Reserve, rose 3.1 per cent in April compared to a year ago, the biggest jump since the 1990s.

But inflation to date has been driven by specific goods and sectors such as used cars, where a “normalisation” is likely as the global economy continues to reopen, said Ivascyn.

In the short-term, Ivascyn is watching rental prices, jobs growth, and long-term expectations as clues for inflation’s next move.

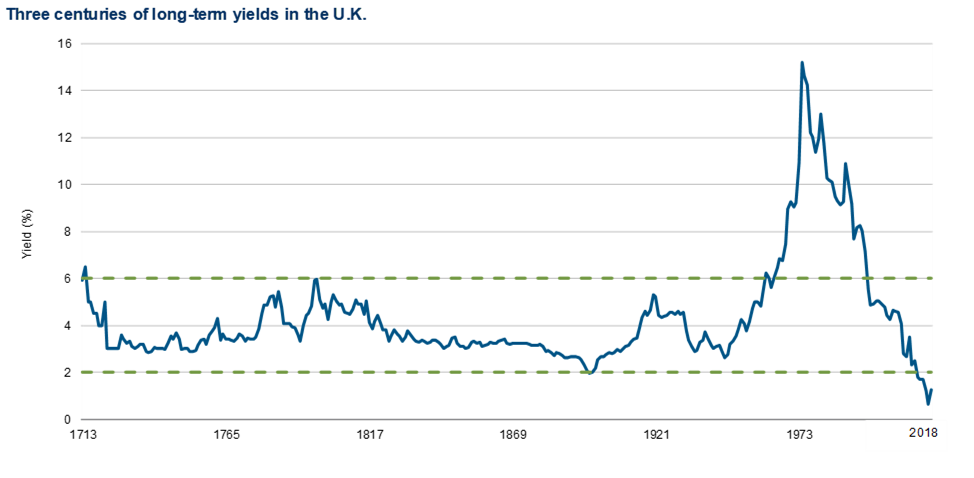

UK long-term bond yields are at their lowest in over three centuries (1713 to today)

Source: PIMCO, Bank of England

{kind=link}

The hunt for low unemployment

Even as uncertainty over inflation continues, policymakers at the Treasury and RBA are increasingly united in their commitment to drive unemployment lower by applying fiscal and monetary policy “for quite some time”, Sivapalan told the conference.

One of the lessons policymakers took from the years since the GFC in 2007-08 was the importance of employment and tight labour markets as “really key” for creating inflation.

“Policymakers have learned from the mistakes of the past and they will push both monetary and fiscal policy for quite some time,” said Sivapalan.

He thinks this newfound aggressiveness could work and see inflation return to levels not seen since before the Global Financial Crisis. He expects this to happen "down the track" and not in the near term.

Ivascyn discussed a similar change in thinking in the US, where policy makers are more willing to aggressively use fiscal policy than in the past.

The longevity of this new approach will be subject to Democrats holding the Senate and House of Representatives in mid-term elections due next year.

Watch the ABCs: Airlines, Banks, and China

Despite “stretched valuations”, cyclical sectors, global banks, and China are all areas of the high yield universe that still offer attractive total returns for fixed income investors, according to Ivascyn.

From a credit perspective, airlines, gaming, hospitality, and certain areas of the high yield market tied to the commercial real estate set are “quite attractive” right now, said Ivascyn.

Global banks also came in strongly thanks to high capital levels and low risk taking. Yields in higher quality parts of the Chinese market also represent a “good source of diversification”.